Sustainability Reporting

On March 8, 2018, the EU presented an action plan for financing sustainable growth, also known as “Sustainable Finance.” This is based on the Paris Climate Agreement, which came into force in 2016, and the United Nations’ 2030 Agenda for Sustainable Development. The focus is on measures to redirect capital flows to limit global warming to well below two degrees Celsius (preferably below 1.5 degrees Celsius) by reducing greenhouse gas emissions by at least 55% compared to 1990 by the year 2030 and promoting the implementation of the UN's Sustainable Development Goals (SDGs) in social, ecological, and economic terms.

To advance and address this relevant topic, new laws and regulations are currently being developed at the European level. Due to the multitude of new obligations, future sustainability reporting will be characterized by high complexity.

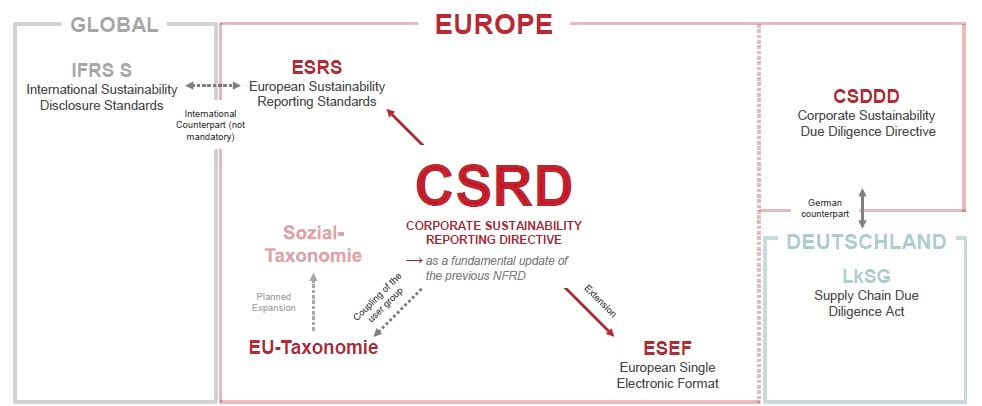

The following diagram illustrates the interrelations of future sustainability reporting.

The CSRD is the core of future sustainability reporting. This comprehensive framework will bring extensive disclosure obligations to a wide range of companies. Further specifications are anchored within the CSRD.

The content of the CSRD is specified by European reporting standards, known as the European Sustainability Reporting Standards (ESRS). These mandatory reporting standards establish detailed disclosure requirements.

At the international level, a counterpart to the European reporting standards has been developed, called the IFRS S Standards. However, according to current legislation, they are not mandatory, unlike the ESRS.

Another specification embedded within the CSRD is the future disclosure format of the sustainability report. Companies are required to provide their sustainability report in a standardized EU reporting format, as defined in the ESEF Regulation.

In addition to the disclosure requirements defined in the CSRD, companies subject to reporting obligations are also required to report in accordance with the EU Taxonomy. This is because the scope of the EU Taxonomy is tied to the CSRD.

The EU Taxonomy aims to classify corporate activities to determine whether they are sustainable. The goal is to direct future investment flows into sustainable activities.

Additionally, there are plans to expand the focus from environmental aspects to social aspects, known as a social taxonomy.

The European CSDDD and the German LkSG define extensive due diligence obligations in the areas of environment and society. The LkSG, which some companies were required to apply for the first time in 2023, focuses on a company’s supply chains. In contrast, the European counterpart, the CSDDD, which is expected to apply for the first time in 2027, encompasses the entire activity chain of a company. Furthermore, the CSDDD goes beyond the LkSG by including civil liability.

Key measures at the EU level include the following laws and legislative proposals:

In Germany, further measures in alignment with EU initiatives are also being undertaken:

Current Information:

- Materials from the Online Seminar on ESG Reporting from November 30, 2022

- Read the articles on reporting under Article 8 of the EU Taxonomy Regulation by Lorson/Metz/Simon, Parts 1 and 2

You may also find this interesting:

- Sustainability Reporting for Public Companies

Your contact persons:

Dipl.-Wirtschaftsjurist (FH) Torsten Ewen

Mainz

Phone +49 (0) 6131 2 04 78 - 52

Fax +49 (0) 6131 2 04 78 - 48

E-mail Turn on Javascript!Turn on Javascript!

Thorsten Kern

Mainz

Phone +49 (0) 6131 2 04 78 - 0

E-mail Turn on Javascript!

Dipl.-Volkswirt Michael Laehn

Mainz

Phone +49 (0) 61 31 204 78 - 51

Fax +49 (0) 6131 2 04 78 - 48

E-mail Turn on Javascript!

Ruchika Mandru-Meyer

Bad Homburg

Phone +49 (0) 06172 18 09 - 0

Fax +49 (0) 06172 18 09 - 40

E-mail Turn on Javascript!Turn on Javascript!

Dr. Christian Metz

Saarbrücken

Secretary's office Jenny Knauber

Phone +49 (0) 681 8 91 97 - 13

E-mail Turn on Javascript!

Carolin Sophie Simon

Saarbrücken

Fon +49 (0) 681 8 91 97 - 47

Mail Turn on Javascript!Turn on Javascript!

Irina Clemens

Bad Homburg

Fon + 49 (0) 6172 18 09 - 0

Mail Turn on Javascript!Turn on Javascript!Turn on Javascript!